This is an excerpt from the latest edition of ‘The Bitcoin Capitalist’: The Bitcoin Effect. Go here to find out what a premium subscription can do for you.

—

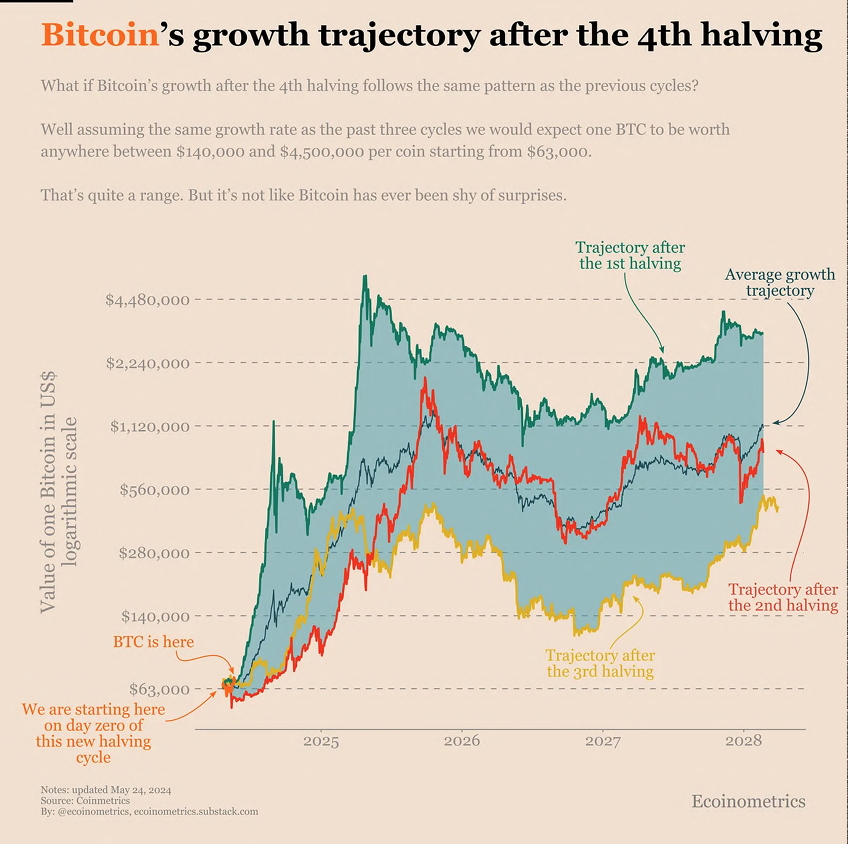

We’re a little over one month since the fourth halving, with the price more or less chopping sideways and the action and sentiment being rather subdued – despite the fact that in terms of immediate post-halving periods, we’re completely in line with prior cycles.

As Ecoinometrics observes,

“Bitcoin is doing ok. No crazy drop. No crazy jump. That’s not surprising. Just in term of patterns, the real growth doesn’t start typically until six months in.

If the macro permits and BTC follows a trajectory within the historical range, one Bitcoin will be worth six figures in 2024. Let’s see how that plays out.”

When comparing prior post-halving moves to where we are now, we’re still on track for a typical year 12-24 month run up.

How high?

It’s always pointless to even guess when it comes to Bitcoin: I’ve been saying a six-digit price is more or less baked in at this point; do we get to seven on this cycle? It’s really hard to say.

Ecoinometrics puts it anywhere between $140,000 USD to $4,500,000 USD – that’s such a wide band as to appear useless at first glance, but what I think both he, and I are saying, is that we’re in all likelihood going to hit six digits (and probably get a good 20% to 30% dump the moment we do), and then it’s within the realm of possibility that we hit seven by cycle end, which I am going to be looking for in Q3 – Q4 2025.

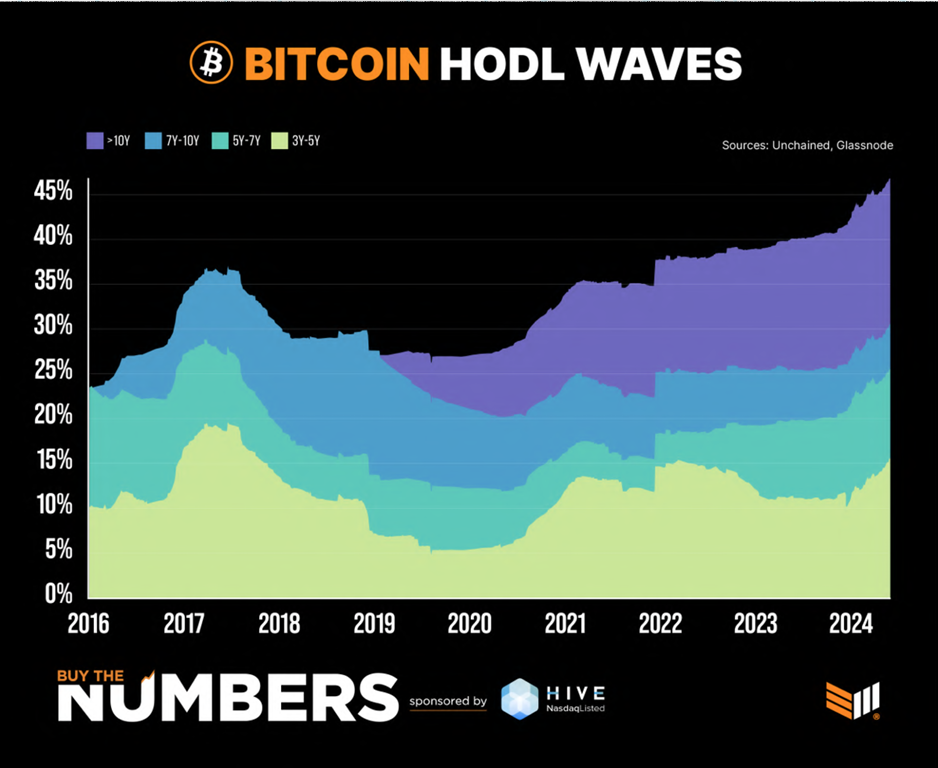

The drivers this cycle are institutions and non-retail players coming in to a market where there is less and less BTC to be had:

For starters, the halving has reduced the new issuance of Bitcoin from 900 new BTC daily to 450. On top of that, the percentage of already existing Bitcoin that has been held in wallets for over three years has been steadily increasing for more than three years.

In fact, if you look at the HODL wave chart (posted by HIVE), you’ll notice that the number of long term-holds is going up across all long-term time frames:

- 3 – 5 years

- 5 – 7 years

- 7 to 10 years

- Even the over-ten-year HODLers are HODLing tight.

The last crypto winter took place over a rare contraction in M2 money supply and a massive drop in M2 growth rate. Bitcoin then bottomed and turned higher – with M2 still coming down.

That was auspicious, because typically, it’s the whole “money printer go brrrrr” narrative that many people think drives the space. With Bitcoin even putting in a couple of fresh all-time highs ahead of the fourth halving, it seems as though we’re coiled for an explosive move higher once things finally kick into gear.

And now, M2 growth rate has reversed and is headed back up – with Goldman’s Mark Wilson wondering if we’re at a “monetary juncture akin to 1995 or 2011.”

via Zerohedge

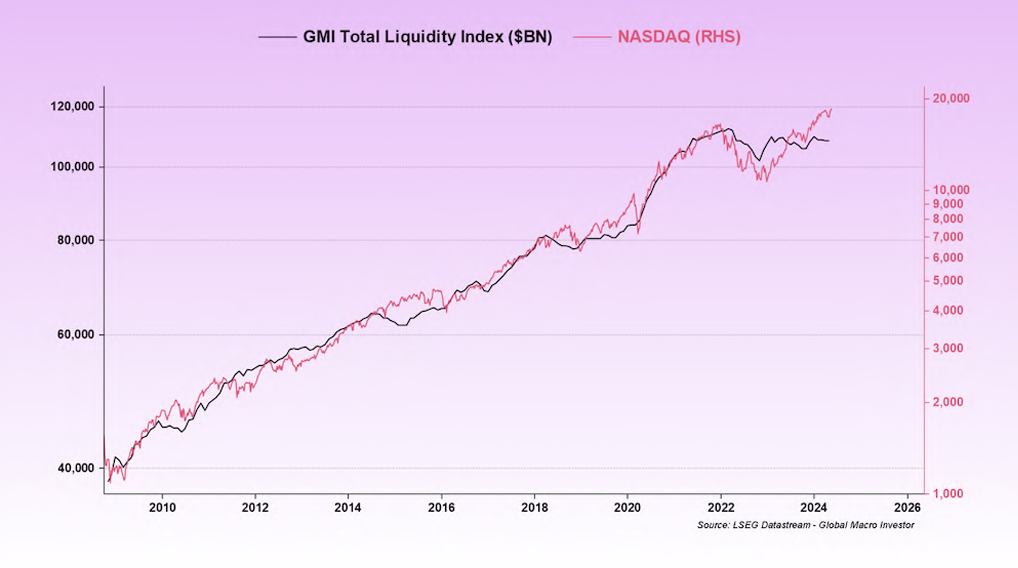

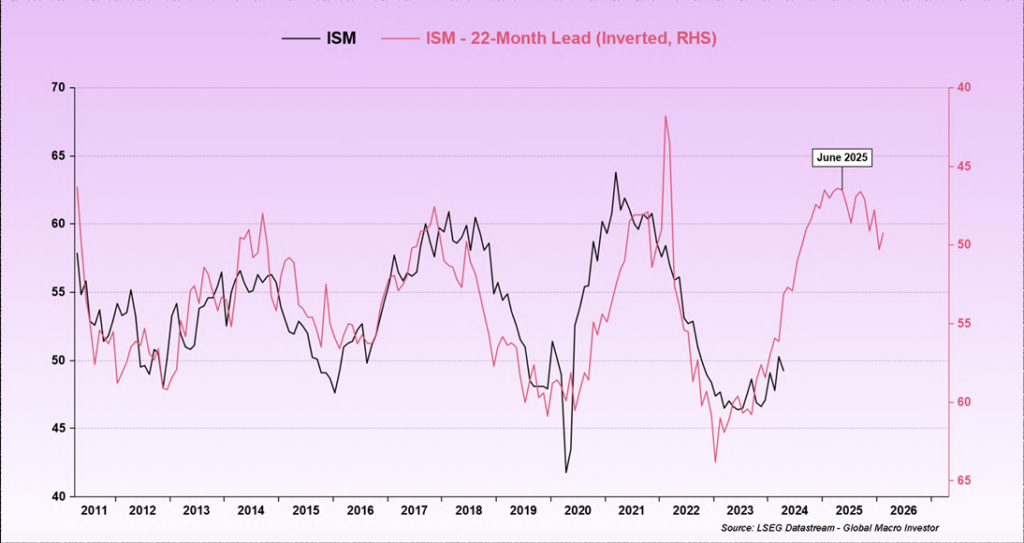

What seemingly drives asset prices higher than outright monetary inflation is liquidity:

And it appears as though all the conditions are in place for liquidity to turn upwards again:

Via RealVision Global Macro

The debt cycle, the election cycle and all manner of systemic pressures on the financial system are aligning to provide an added boost for this cycle (and it may be the mother of all boosts).

The first order consequence of the liquidity cycle (or perhaps more accurately, the driver of it) are central bank balance sheets, which just keep expanding and as far as I can tell, well never meaningfully revert to pre-pandemic levels, let alone where they were before the GFC.

Raoul Pal frequently alleges that during the GFC, the central banks of the world made a deal to absorb all the bad debt onto their own balance sheets, and from that point on, CB balance sheets will just continue to soak up any speed wobbles in the global economy.

That’s why PE multiples for equities remain at nosebleed levels – and why things like value investing no longer works.

Zoltan Pozsar came to the same conclusion, albeit from a different angle, saying value investing is dead “because bonds offer no value”.

He says that until bond investors impose discipline onto the bond markets (demanding some manner of “margin of safety”) – then as long as central banks backstop the debt markets (see balance sheet talk, above), asset prices will continue to rise. No discounts, no mispricings relative to value, no margin of safety – just all risk premium, all the time, as discipline gets thrown overboard.

(Yes, I frequently describe myself as having come up a value investor, but I finally began to realize that “the system” will never again allow the financial markets to come unglued to the point where deep value exists. It happens, but it’s rare – and also notable is that the one place we seem to find it, from time to time, is in crypto, when we uncover equities trading below the mark-to-market value of their digital assets).

—

This is an excerpt from the latest edition of ‘The Bitcoin Capitalist’: The Bitcoin Effect. Go here to find out what a premium subscription can do for you.