“You just wait until the next bear market…”

Last month, I talked about how many of the legendary investors I’ve long followed as well as many of my contemporary financial commentators (speaking specifically of the contrarian ilk), are almost unanimous in the opinion that the AI trade is well into bubble territory and stocks in general are overvalued. Hell, even I think that and I’m personally “all in” on AI and have a fair bit of equities exposure to it (not a tonne, but it’s there, and the biggest winners in the TSC portfolio lately have all been AI stocks and HPC stocks).

Angela sent me this Diary of a CEO interview with Jeremy Grantham – another legend – and she said it was scary. At his peak he managed something like $165B AUM, but he’s down to $80B or $90B now (he also says the only reason he’s still counted as a billionaire today, personally, is because they include the money he’s given away. Grantham has donated over 90% of his net worth to the Grantham Foundation, which invests and incubates primarily green-tech innovation to combat climate change.

Although Thomas Braziel, whose name you might recognize as a notable distressed asset investor who specializes in crypto i.e. Mt Gox claims, FTX, put out an interesting analysis of Grantham’s green tech foundation’s filings – and surmised that what he’s saying on the talk-show circuit isn’t lining up with where he’s actually allocating the foundation’s …money 🤔 )

Grantham occupies an exalted perch in the pantheon of institutional investors, so when he opines on something, it tends to get picked up on, which one may find somewhat quizzical, given his lifetime batting average isn’t really in the same league as the likes of Buffet, Munger, Klarman, et al.

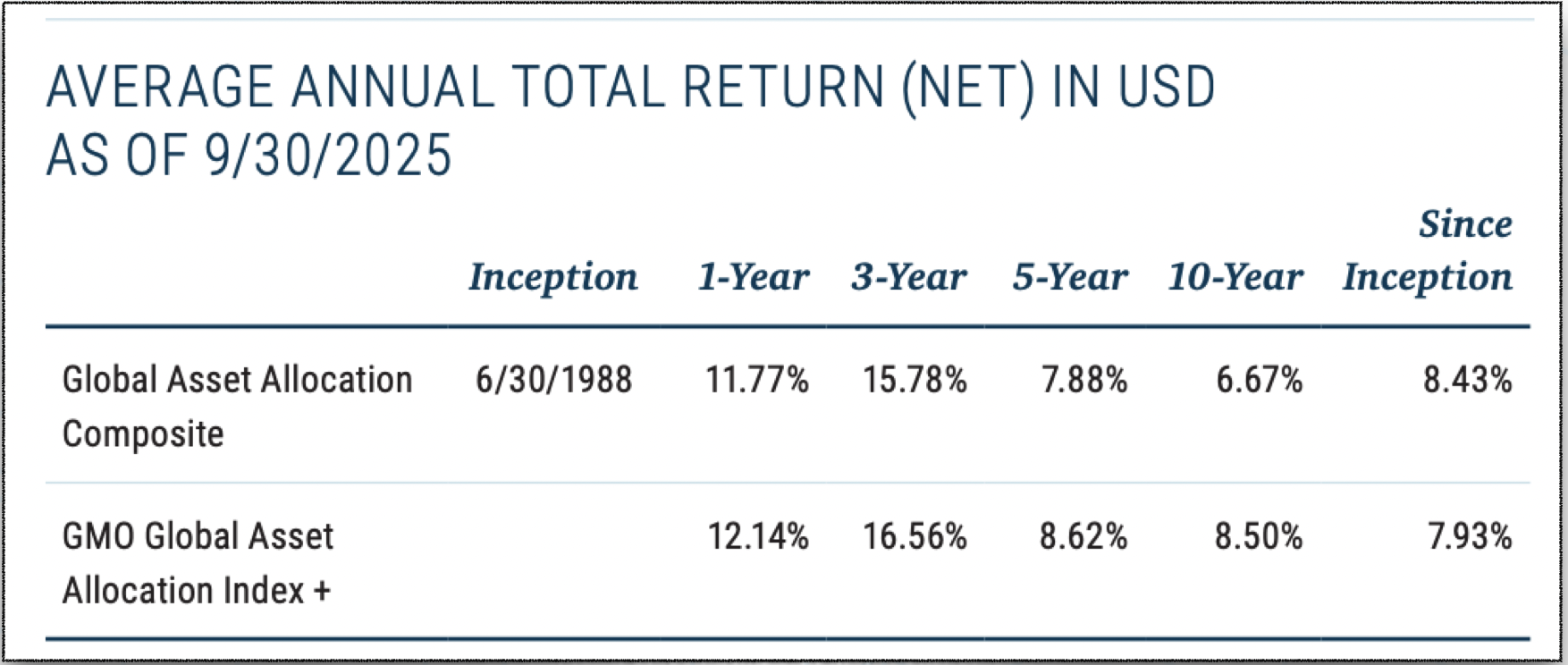

His lifetime average returns? The closest analog could be the lifetime average of the GMO Global Asset Allocation Composite, which he co-founded.

Their number? 8.43%. And 0.8% of that was because of a one-time litigation settlement received in 2024

Warren Buffet’s lifetime batting average is pushing 20% (19.8%).

The S&P itself, 10%.

In case you’re wondering how somebody became a billionaire by lagging the major index by 200bp over their entire career, it’s because Grantham is proficient at one thing in particular: not losing money.

The TL;DR from the DOAC interview? A lot of people are about to lose a lot of money.

When Stephen Bartlett told him he was invested in SpaceX, Grantham dead-panned, “Good luck with that”.

Bitcoin? “It’s a zero”.

The interview went a bit viral and I saw a lot of “Billionaire says Bitcoin is worthless” headlines in the mainstream financial press. Grantham has since been on a punditry tour (perhaps in promotion of his latest book, “The Making of a Permabear” – yes, really); and the soundbites that are being repeatedly teased out from them are his “Bitcoin is a zero” sermons, in one case getting into a somewhat heated exchange with Joe Kernen on CNBC – where Kernen, incredibly, makes some of my points far less diplomatically than I have here.

At least it’s not just Bitcoiners getting into scraps! pic.twitter.com/pfJyXM3ZFc

— JOEY (@JoeyTweeets) June 26, 2026

After Grantham trotted out the usual “no use case”, “there’s no there there”, “it’s a bubble”, Kernen straight-armed Grantham in the face with his underperformance over the past two decades,

“You’ve done a great disservice to anybody who’s listened to you over the last twenty years”.

Grantham’s response and attempt at a defence, combined with something else he said in the DOAC interview, are all leading up to my point here, while being 100% oblivious to it:

To Joe Kernen: he said “We’ve been in a bull market since 2009, let’s see how all this stuff holds up when the next bear market hits”

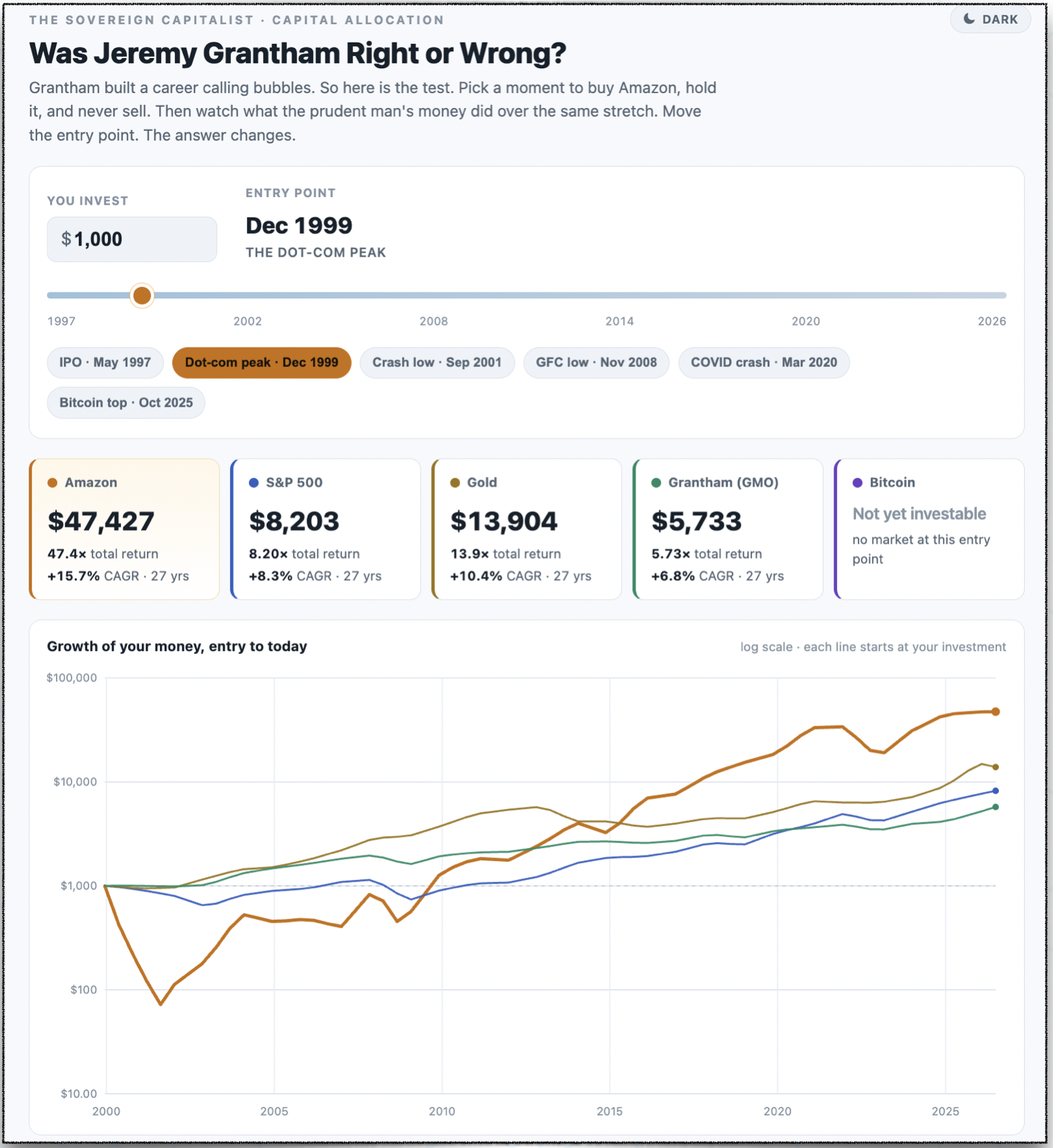

To Steven Bartlett: he cautioned how Amazon sold off a staggering 92% during the Dotcom bust.

During the drive to Hamilton for a board meeting, I listened to this short Alex Hormozi clip and his analogy (which he cribbed from Brian Johnson) hit me full force and I finally had a working metaphor that explained what I’ve been trying to articulate about these living legends of finance.

That they’re underestimating the significance of fiat debasement is true, but it doesn’t really explode in your brain as much as make your eyes glaze over.

The analogy is fish are swimming around in water. Some of them become experts at swimming. They train their entire lives, they practice every day, they study the expert swimmers of yore, and they analyze nearly every aspect of the water they inhabit: it’s PH levels, alkaline, currents, flow – everything.

They know how a slight variance in one factor impacts the others – they know “which way the current is going”.

But over time, the water heats up; they may pick up on this, but they’re never quite prepared for what it means beyond a certain point.

When that point arrives, the water evaporates – and now it’s gas. Steam.

Setting aside for our purposes how this would fry the fish, imagine they’re still alive, but now they’re trying to apply everything they know about swimming in water to this new environment, which is gaseous, not liquid.

They would be flailing and flapping around like the proverbial “fish out of water”.

What happened?

They were never wrong about their fluid dynamics.

The physics changed and they had no model for the new reality.

Hormozi’s short clip was applying this metaphor to AI – which is certainly among the key drivers of the “monetary physics change” that we are now undergoing.

But the point of no return, when the phase shift started, was – I believe, and as Raoul Pal has always said – the Global Financial Crisis of 2007-2009.

That was when the water started turning to gas.

Grantham’s own yardstick measures the current bull market from then – when the central banks stepped in, when The Big Print started and when interest rate suppression and credit expansion became permanent features of the global monetary system (I would argue that the process started in 1980-82, and the GFC was a major tipping point).

Yes, Amazon came off 92% when the dotCom bubble burst. But anybody who had bought, even at the high right before that, is now up about 4,642.7 %

On the new Sovereign Capitalist site, we can model all this out interactively (see below).

On its surface, Grantham’s fixation on loss avoidance serves a purpose (recall Buffet’s top rules of investing: number one is “Don’t lose money”, number two is “See Rule number one”).

If I ever experienced a staggeringly huge life-changing windfall in one moment, I would carve out a “retire your bloodline”-type allocation and hand it to a guy like Grantham (more likely it would be Vito Maida over at Patient Capital, here in Canada).

But being good at preserving capital has its own opportunity cost, which is far more pronounced now that we’ve traversed the inflection point into the Exponential Age.

The world has transitioned from flat to hyper-cubed – the architecture is completely different now, and the linear measuring stick known as fiat money is ill equipped for the task of describing it.

To Grantham’s point “you just wait until the next bear market”, there won’t be a next bear market, not until we change that measuring stick.

Until the monetary regime change happens – that “change in physics” – any drawdown, no matter how deep, will be papered over with incessant Big Prints until the system itself completes its metamorphosis.

Today’s post was an excerpt from The Sovereign Capitalist my recently relaunched premium service. This goes beyond a dashboard, it’s more of an operating system for high agency net-producers. All members get access to the full pre-release version of my new book: The Blueprint – Survive & Thrive in an Overclocked Timeline.

Try it out for a month for $7, when you use the promo code TSC_PREVIEW26 here.