Paul Krugman took time out from his European vacation to write why he’s a cryptocurrency skeptic. This is not surprising given who he is and what his positions have been over his career. Most of the orthodox criticisms against cryptocurrency I covered previously in my “This Time is Different: What Bitcoin Isn’t” and “What Bitcoin Actually Is” series. But it’s worth recounting how one could easily take many of these criticisms against Bitcoin, search and replace “bitcoin” or “cryptocurrency” for “US dollar” and come out with are more applicable criticism of the modern fiat money system.

“Cryptocurrencies, by contrast, have no backstop, no tether to reality. Their value depends entirely on self-fulfilling expectations — which means that total collapse is a real possibility. If speculators were to have a collective moment of doubt, suddenly fearing that Bitcoins were worthless, well, Bitcoins would become worthless.”

This is more or less a truism that can be said about any fiat currency. Krugman seems to not notice, or care, that for most of recorded history, most currencies were either hard currencies (gold, silver, etc) or hard backed. Elastic, fiat currency, worldwide has only been around since the 70’s, and here’s Krugman complaining that it’s Bitcoin that has a tethering problem (or lack thereof). Further,

“In normal life, people don’t worry about where the value of green pieces of paper bearing portraits of dead presidents comes from: we accept dollar notes because other people will accept dollar notes. Yet the value of a dollar doesn’t come entirely from self-fulfilling expectations: ultimately, it’s backstopped by the fact that the U.S. government will accept dollars as payment of tax liabilities — liabilities it’s able to enforce because it’s a government.”

But people do lose faith in both currencies and governments. There have been 21 hyperinflations over the last 25 years.

It’s happening right now in Venezuela, where the inflation rate is on track to hit 1,000,000% by the end of the year, and Turkey may be next up.

Cryptocurrencies, meanwhile, are tethered to math. While in Krugman’s own words, fiat currencies can be created out of nothing:

“Instead of money created by the click of a mouse, we have money that must be mined — created through resource-intensive computations.”

Yes, that is entirely the point. In a recent Peak Prosperity podcast Chris Martenson quoted Charlie Munger’s observation: “show me the incentives and I’ll show you the outcome”.

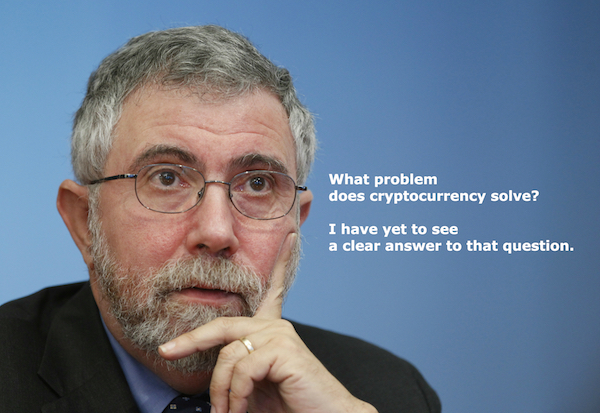

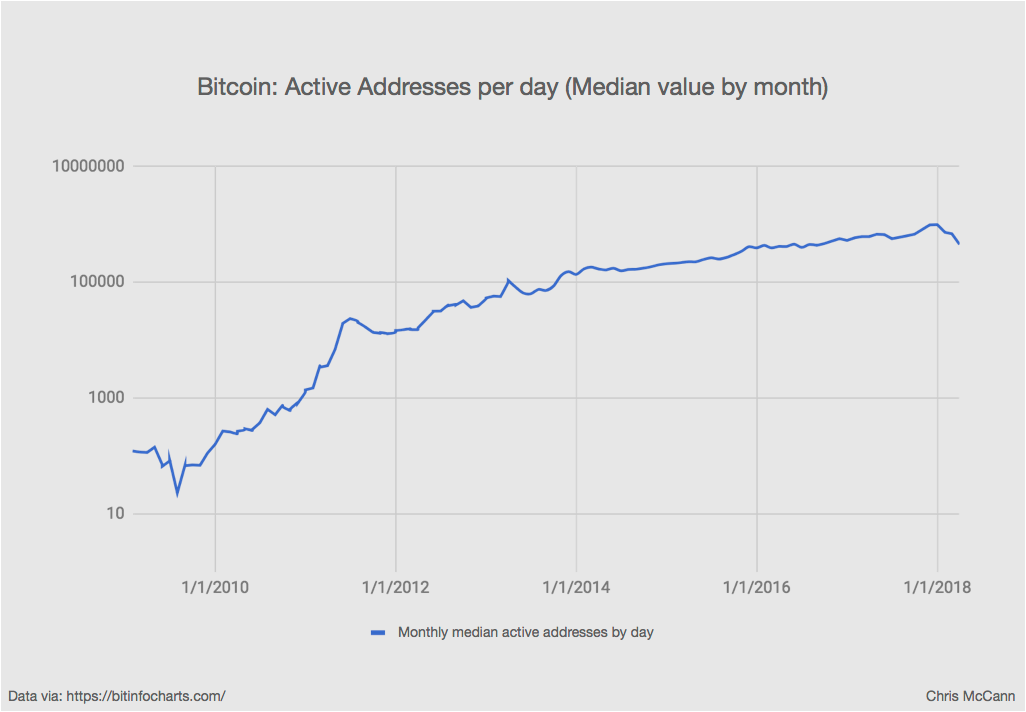

Krugman wonders “What problem does [Bitcoin] solve? I have yet to see a clear answer to that question.” Maybe we can clarify things by starting with the outcome: the fact that cryptocurrencies are here and as the data shows, steadily gaining traction, and then work backwards. (By gaining traction I’m not even talking about price action of any given cryptocurrency, I mean usage-based metrics like transaction volume, active addresses, hashing power, etc)

When we work backwards we can arrive at what the incentives were that gave rise to this phenomenon. When we do so we’ll understand that they didn’t spontaneously arise out of whim, they came about for a reason, and those reasons are the problems that crypto solves.

Crypto’s 7 Mothers of Invention

1) The custody problem

The custody problem is what we can call any situation where your wealth can be confiscated from you without your consent. I mean this in a sense distinct from outright criminal activity. All assets, crypto or not, have vulnerabilities to theft. Ostensibly we have legal recourse under our justice system to seek redress and punish wrongdoers. That isn’t the custody problem, the custody problem is when, for whatever reason, money or assets that belong to you are taken away in a manner that is then deemed to be “legal”.

A key example of this was the Cyprus Bail-in, which was the first time Bitcoin started making headway into the public consciousness, where it quadrupled in value when Jeroen Dijsselbloem described what was about to happen as a template for future bank recapitalizations across the Eurozone. People began to realize two things:

A) maybe central bankers around the world weren’t able to control the economic destiny of the Universe, and

B) next time some banks blew themselves up they were going to be recapitalized with depositor funds.

Other events followed, from “bail-in” language being introduced in legislation from Switzerland to Canada, to MF Global imploding to the chagrin of unit holders who found that their accounts had been rehypothecated from under them.

Suddenly cryptocurrencies were looking like an idea whose time had come, so long as one holds their private keys themselves (cryptos understand implicitly: not your keys = not your coins).

2) The capital control problem

This is related to Problem 1, only instead of your being stripped of your wealth through confiscation or rehypothecation, you get trapped inside a system you have no control nor lattitude, or else chased into assets you’d otherwise not want to be invested in.

Cryptocurrencies slip through capital controls with ease. I was having a hard time wondering what Krugman was talking about throughout his piece about how hard and expensive and slow it is to do Bitcoin transactions, and yet, you can move hundreds of thousands or even millions from address1 to address2 for a few dollars in timeframes ranging from seconds to hours.

Meanwhile, wire transfers, still, to this day scare the living crap out of me every time I have to send one because it takes as long as a week just to find out that it hasn’t arrived and nobody has any fucking idea where the money is. Sure, it’ll get wound back, eventually. But that doesn’t exactly strike me as frictionless. These aren’t edge cases either, anybody in business knows this happens often enough that you end up worrying about it all the time.

China is a great example of a totalitarian police state with ubiquitous state surveillance, an absence of civil liberties and capital controls. Ironically, China is also one of the giant sources of hash power for crypto mining.

3) The dilution problem

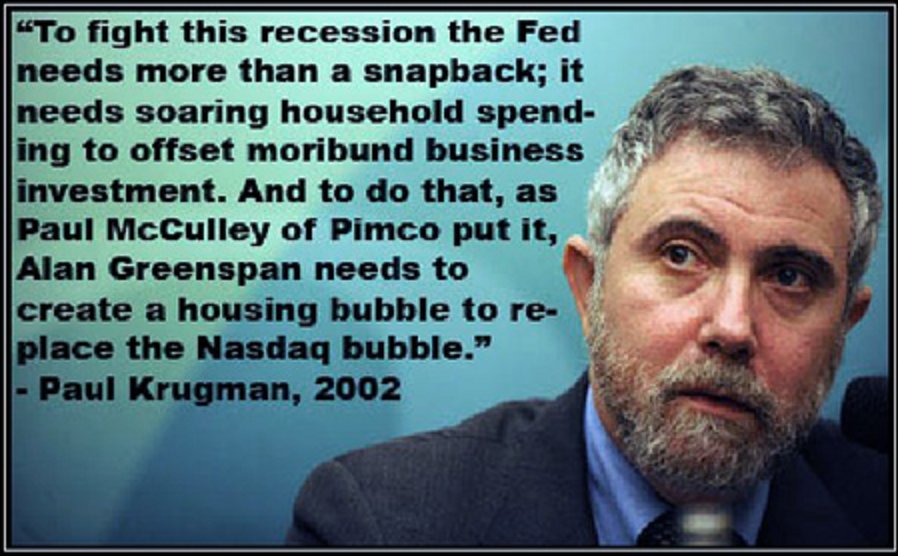

It bears repeating what Krugman likes about conventional money: you can create it with a mouse click. Well you can’t. The Fed can. The money centre banks can. That’s a pretty sweet deal, if you own, run or are otherwise comfortably cozy with a bank or the Fed.

Most of us aren’t, so what happens to the rest of us is that we have to compete with the privileged few who get direct access to this freshly minted money. Only we don’t get to use freshly minted money, we have to use our own money, that we actually earned, somehow.

The stock market bubble, tech unicorns, the entire fracking industry, it’s all built on money centre banks receiving freshly minted money and ramming it into private equity, investment banking, venture capital, and financialization – in other words, blowing up asset bubbles that have had one singular, defining effect that will take generations to unwind: acute wealth inequality and the decimation of the middle class.

If you don’t believe that this is a problem let’s take a single example of this dynamic in action. Yesterday, as I started writing this, Apple became the first company in history to achieve a trillion dollar market cap. One of the largest shareholders in Apple, is the Swiss National Bank. The SNB became one of Apple’s largest shareholders through it’s Swiss franc stabilization regimen. That’s where they print Swiss francs out of thin air, sell them for Euros and then use those Euros to buy up assets, including shares in companies, including Apple. Here we have the microcosm example of central bank money printing contributing to currency debasement and asset bubbles in one shot. This isn’t an outlier, it’s the way the system is constructed right now.

Every dollar that gets printed dilutes the value of every dollar we worked for, earned or saved. As I remarked previously

“debt-based inflationary money creates a treadmill economy, which perniciously pushes assets up the wealth inequality ladder, as the Plutocrats on top spend their compounding wealth on buying up assets, while the lower tiers (the non-super rich) must continually and incrementally spend more of their purchasing power on staying alive.”

Cryptocurrencies by contrast are inelastic, deflationary currencies. Price volatility aside, which I think can be ascribed to it still being early days for crypto, the overall effect is that units gain purchasing power over time. As I noted in my earlier series on Bitcoin, there’s nothing wrong with a deflationary currency as long as you’re not using debt for money.

( I expanded on this a lot more in my review of David Golumbia’s Politics of Bitcoin book, wherein he attempts to dismiss any criticism of inflation as far-right extremism but even a cursory examination of his thesis shows beyond a doubt: inflation erodes the currency, either quickly or gradually, whereas crypto-currencies demonstrate anti-fragility and gain value over time)

4) The consensus problem

What I mean by “the consensus problem” is that consensus should describe a state where all affected parties to a transaction or a system should be voluntarily consenting to participate. There’s a problem when things are structured such that some participants are favoured, say by receiving freshly minted money before the effect of that new money dilutes everybody else’s purchasing power or by artificially holding interest rates below their market clearing values for over a decade thus rewarding debtors at the expense of savers.

The consensus problem arises when we’re forced to play a game that’s rigged against us, whenever the people in charge of the state or the money supply take it on themselves to change the incentives, give those closely affiliated with themselves preferential treatment or more generally pick winners and losers.

With cryptocurrencies, consensus is voluntary and participatory to the extreme. Nobody takes part in a cryptocurrency ecosystem with a gun pointed to their head. Then if people don’t like the direction something is going they can just “fork off” and go their own way with things. A good example of this functioning in a perfectly smooth and rational manner was the Bitcoin Cash fork of Bitcoin Core, or even Ethereum Classic’s fork from the Ethereum Mainnet.

Sure, there may be intense animosity between the rival factions, they didn’t go their separate ways because the affection and camaraderie was too intense. But they each took their irreconcilable differences and decided to try to run things in their own way, and from there the market forces take over. Not a single shot was fired not one bomb was dropped.

This is what a free market system actually looks like.

5) The “BUMMER machine” problem

When Krugman talked about how clunky and expensive transactions were he was probably referring more to day-to-day commerce and ecommerce activity than in moving larger sums of capital around. I hear a lot of people complaining about that, but when you drill down I can’t find many complaining about it that have actually ever done a cryptocurrency transaction.

I walk around with a couple of wallets on my mobile device and I routinely use them to spend crypto, at conferences, or even on websites. It varies, sure maybe in some cases the wait for confirmations will take longer than a credit card transaction, but again, early days.

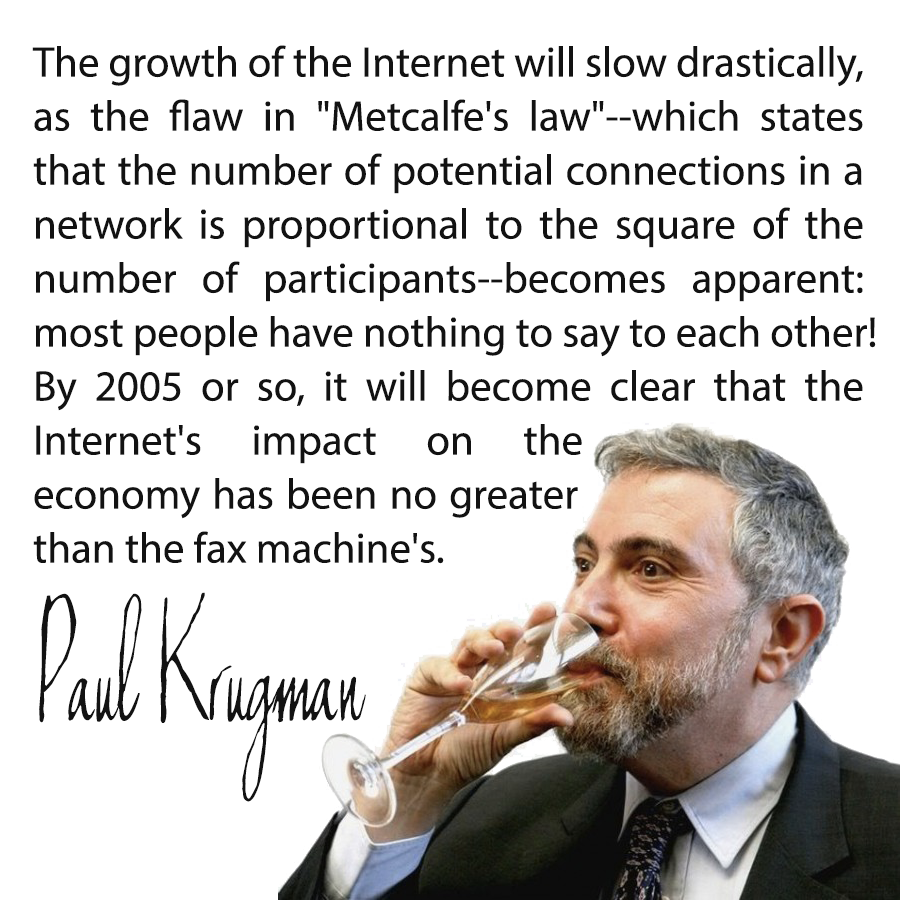

Further, I remember having to wait for GIFs or songs to download, nevermind HD streaming over the wire. Things get faster. Remember, we’re dealing with a guy who figured the internet wouldn’t have much more impact than a fax machine so his take on technology isn’t the most prescient.

But one thing the Internet economy has been pining for since the very beginning is a viable system for micropayments. Online credit card transactions isn’t it, neither is PayPal or anything where you have a minimum transaction size measured in dollars and transaction fees larger than what a micropayment would be. Micropayments will drastically change the dynamic of the internet economy. If you read Jaron Lanier’s Ten Arguments For Deleting Your Social Media Accounts Right Now (excellent read, highly recommended and I will be reviewing thoroughly in my next post), he calls the current ad driven internet ecosystem “The BUMMER Machine”, which breaks out into 6 parts under the following mnemonic:

A is for Attention Acquisition leading to Asshole supremacy

B is for Butting into everyone’s lives

C is for Cramming content down people’s throats

D is for Directing people’s behaviour in the sneakiest way possible

E is for Earning money from letting the worst assholes secretly screw with everyone else

F is for Fake mobs and Faker society

— Jaron Lanier “The BUMMER Machine” in “Ten Arguments For Deleting Your Social Media Accounts Right Now”

BUMMER puts a point to that Munger observation: “show me the incentive, I’ll show you the outcome”. When the incentives are attention, clicks and eyeballs, the outcomes are dumpster fires of clickbait, ubiquitous tracking and invasions of privacy.

Cryptocurrency systems like Brave are bringing micropayments closer to reality and that will disrupt the ad-based revenue models of Facebook, Twitter and Google as much as Uber disrupted the cabs or Ebay disrupted the pawn shops. It’ll be a wrecking ball, and that wrecking ball will demolish the BUMMER Machine.

6) Execution problems

The plot lines in the latter half of The Big Short, the dramatized version of the Micheal Lewis book once the hero protagonists were no longer being laughed out of offices as cranks and were now vindicated by their predictions coming true, they found themselves with a new problem:

Their counter-parties were flaking out on them.

During that same period legendary short-seller https://bombthrower.com/wp-content/uploads/2019/03/shutterstock_1030471843-e1551983495127-1.jpg Cohodes encountered similar issues when the financial institutions arbitrarily hiked his margin requirements despite his being on the right side of his trades as the companies he had bet against were imploding. Despite his short thesis being bang on, the hi-jinx forced him out of his trades to the point he had to wind up his hedge fund.

When it comes to banks as counter-parties they seem to operate by a “heads we win, tails you lose” playbook. With blockchain platforms like Ethereum and EOS we get financial instruments, or rather smart contracts which have guaranteed execution built-in. There wouldn’t be any changes to the rules after all parties sign with their keys, when that happens, all bets are on. No matter what.

Thus, derivatives would not be created without proper collateraization or if they did, the consequences of that would be borne entirely by the counterparties involved.

Krugman might argue that precludes creation of synthetic derivatives that a lot of the banks today rely on. But again, that’s the point. If toxic derivatives nearly destroyed the entire world economy in 2008, then wouldn’t you describe a system that makes proliferation and amplification of those instruments impossible as having solved another problem?

7) The moral hazard problem

Moral hazard is when somebody passes on their risk to somebody else, without that somebody else knowing, or willfully accepting that risk. An example would be when a bank gets itself into trouble and then gets bailed out by the government or the taxpayer, or gets recapitalized through a bail-in.

When the current imbalances, built up over 10 years of ZIRP and NIRP come home to roost and the next financial crisis hits, when the government bails out the parties again or opts to confiscate yours and my wealth to recapitalize a failed system, it will be another example of moral hazard. They make the stupid policy decisions and enforce them, at our expense; and then we get to pay for it when it all implodes.

We’ve already seen the equivalent of insolvent banks and had several financial crises within the crypto-currency space and moral hazard wasn’t much of an issue.

When Mt Gox failed, it went down and that was it. It was blinking bright red warning lights for months and anybody who was paying attention acted on it and anybody who didn’t got wiped out. Karpele didn’t get a bailout out of which he paid himself a handsome bonus. Gox was put into bankruptcy and Karpele found himself facing some questions and courts around the world. This is the way it was supposed to work.

To sum it briefly, as I observed in my review of Politics of Bitcoin:

“Bitcoin is a movement born from protest. If the people behind it thought that the monetary system was fairly structured, that those who control it exercise legitimate power to the benefit of wider society and that an egalitarian democratic ideal was at work, functioning largely as intended; then nobody would have bothered to invent it.”

In other words, if cryptocurrency didn’t solve anything, it wouldn’t exist.

At the very least, crypto-currencies can protect us from the problem of policy makers taking advice from academics with zero real world experience like Krugman and enacting policies to implement their hare-brained economic models….

Mr. Jeftovic,

Many good points here. I’m no economist, but I see a bit incorrect (or maybe imprecise) here and there; a lot of would-be economists make similar imprecise points. One item that could be misinterpreted:

“Every dollar that gets printed dilutes the value of every dollar we worked for, earned or saved. As I remarked previously

‘debt-based inflationary money creates a treadmill economy …”

I would think the current absurd debt-based monetary system has a deflationary mechanism since when conjuring up new money as commercial ‘loans,’ they don’t create the money with which to later pay the interest being demanded, and therefore if new money supply wasn’t being created faster than required by repayments of debt principal along with interest from ‘somewhere else,’ existing money would become more and more scarce, thus more valuable, since final payment of the principal results in the originally-conjured money being extinguished. (Meanwhile the ‘original loan’ in question has been re-deposited and multiplied many times by down-the-line banksters maintaining only fractional ‘reserves.’) But if the money supply were expanded by just the right amount during any given time period to nullify the former deflationary effect while avoiding inflation elsewhere in the monetary circuits by not expanding money supply excessively, theoretically there need not be inflation, I’d think. Of course, since the banksters at the top control the system firstly for the benefit of themselves and their fellow ruling-class cronies, greed/hubris/misanthropy/etc take over and allow money supply expansion far beyond what’s required by any real increase in humanly-beneficial [national] economic activity, we get inflation, volatility and booms/busts, etc. Also, of course most of the money in circulation never gets printed physically, but is only blips on some computer. The formulas by which this system is maintained assume endless expansion, endless growth: the ethic of the cancer cell, which tends to grow until it destroys both its host and itself. That’s compound interest for you: no relation to the real world, but a reliance upon disembodied mathematics which leads to real-world instability and has to be artificially cut short somehow. In recent centuries they’ve increasingly resorted to wars to destroy what was previously produced and then consume more bankster-created credit in order to rebuild, but war is essentially obsolete (although society hasn’t really realized that yet), so the war outlet becomes less and less tenable. The old system may be running out of options, leading to desperate measures. Can one or more new cryptos supplant and eventually replace fiat currencies? They would have to be elastic, which most aren’t (yet), to expand or contract based on total economic activity of a given set of people. Although Bitcoin is a pioneering effort, its “proof of work” mechanism is an inherently artificial and wasteful inefficiency which can’t scale to nationwide or planetary level, so we must look elsewhere for a better solution to the treadmill economy which creates temporary opulence for a few and longer-term misery for the masses.

1) Bail ins. Bail ins are and will be common in crypto. Several days ago, someone had futures long position for $415 million on OKEx and lost great deal of money. Losses were spread between profitable customers. Earlier when Bitfinex was hacked, losses were spread between customers. It’s not a bug, it’s a feature. US futures exchange are backed by consortium of largest banks that has never failed. Bitcoin exchanges are not capitalized well and this will happen over and over.

3) Dilution. Central banks dilute sometimes. Sometimes they do the opposite –withdraw liquidity. That is happening right now. Bitcoin dilutes always, every second of its existence. Because only by dilution real electricity expenses of miners could be paid. Again, its not a bug, its a feature.

4)Rigged system. Bitcoin is the most rigged system that was allowed to exist in modern times. Bitcoin anonimity makes it an ideal vehicle for fraud and manipulation of markets. Any kind of insider trading, collusion, painting the tape, self dealing, front running — any scam that ever existed in trading is undetectable here and is rampant.

5) Micropayment. How is Bitcoin suitable for micropayment? Why wait 10 minutes for miners to compete to get a long hash with your block and waste time and money for you fraction of a cent payment? How could it conceivably be cheaper than just doing it through paypal that doesn’t have all these overheads? Why do so much work if you don’t give a damn of anonimity of your micropayment?

6) Execution in derivative. This makes zero sense. The same derivative brokers who played games in 2008 manage Bitcoin futures trading — futures trade on CME. They are regulated by the same government that could play the same games. Like ban shorts and cause short squeeze. Why wouldn’t they play the same and worse kinds of games?

7) Moral hazard. Yeah, you said it yourself — when there is fraud or hack or anything in bitcoin you are on your own. You are wiped out. There is no insurance, like it is with a bank account. It’s better for the taxpayers, granted, but not for Bitcoin holders. I guess you are saying that if someone is reckless enough to put money in bitcoin, let them take one for the team. This is your only point that i agree with.

Thanks for the writeup. Your 4) didn’t quite hit the target: Monopoly. Or stated otherwise, control the flow of credit and you don’t care who makes the laws. You either have a Monopoly or you don’t, and now, post Bitcoin, “they” don’t.